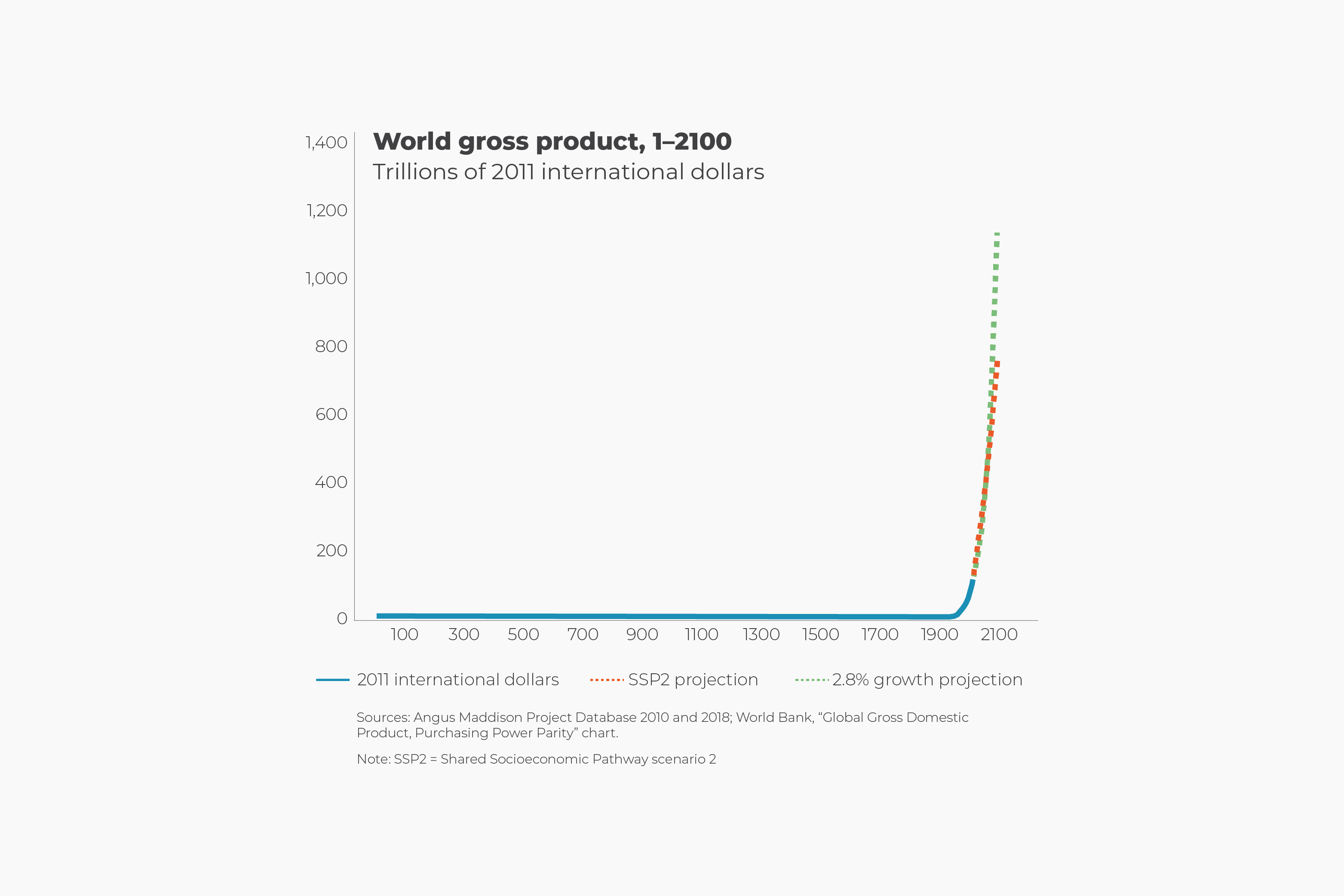

Since 1820, the size of the world’s economy has grown more than a hundredfold. Over the past 200 years, the world population grew somewhat less than eightfold. Measuring the size of the economy over time is challenging, however. One commonly used measure is the 2011 constant international dollar, which is a hypothetical unit of currency that has the same purchasing power parity value that the U.S. dollar had in the United States at a given point in time. Economic growth figures are adjusted to reflect the local prices of products to give a better idea of the purchasing power of individuals in different countries over time.

Between 1500 and 1820, world gross product grew about 0.3 percent per year, eventually tripling from $430 billion to $1.2 trillion. As some countries began adopting freer markets and the rule of law spread along with increased international trade, the pace of global economic growth sped up to 1.3 percent annually, increasing the size of the world economy to $3.4 trillion in 1900. Since that time, global economic growth has averaged slightly more than 3 percent per year, boosting world gross product to more than $121 trillion by 2018.

What about the future? The Intergovernmental Panel on Climate Change’s (IPCC) benchmark middle-of-the-road scenario—which features medium levels of economic and population growth—projects that the global economy will grow to about $600 trillion by 2100. The IPCC expects that the global economic growth rate will average about 2 percent annually in that scenario. If, however, global economic growth were to maintain its 2.8 percent average rate since 2000, the world’s economy would instead increase by almost tenfold to $1.1 quadrillion by 2100.